2.png)

UAE’s New E-Invoicing System Explained: Ministry of Finance Policy Breakdown & Business Impact

Table of Contents

About the Author

The author is a compliance specialist with expertise in UAE business regulations, corporate governance, and financial compliance. They focus on helping businesses navigate regulatory changes, stay audit-ready, and implement best practices in areas such as invoicing, taxation, and reporting.

Key Takeaway:

- UAE’s new electronic invoicing framework goes beyond formatting, it transforms how invoices are generated, validated, transmitted, and archived, affecting ERP systems, cash flow timing, VAT accuracy, and operational workflows.

- Delaying readiness exposes businesses to ERP compatibility issues, invoice rejections, penalties, and operational bottlenecks. Companies that start assessments, data cleansing, and ASP integration early experience smoother transitions and fewer compliance gaps.

- Successful implementation requires collaboration between finance, IT, compliance, and audit teams. Structured e-invoicing enables process discipline, improved reporting, stronger internal controls, and can even drive operational efficiency beyond mere regulatory adherence.

Why E-Invoicing isn’t Just a Format Change

When VAT was introduced in 2018, many UAE businesses underestimated the operational impact. Whilst working with a Dubai-based trading group that believed their ERP system was fully VAT-ready. During a pre-audit review, we discovered incorrect zero-rating logic coded into their system, exposing them to over AED 1 million ($272,295) in potential tax adjustments.

That experience has taught us one important lesson: regulatory changes rarely affect “just compliance.” They affect systems, processes, cash flow, and risk exposure.

Recently, the UAE Ministry of Finance issued new electronic invoicing guidelines, introducing a structured digital reporting framework for VAT-certified businesses. This development is more than a format change, it represents a shift in how commercial transactions are validated and reported in the UAE.

In this article, we will explain what the new framework means, who must comply, the technical and operational impacts, and what businesses should be doing now, based on our experience over a decade of advising UAE companies through VAT implementation, audits, and regulatory transitions.

Who this Article is For

This analysis is particularly relevant for:

- CFOs and Finance Directors

- VAT-registered SMEs and corporates

- Free zone businesses making taxable supplies

- ERP and IT managers

- Tax and compliance officers

If your company issues VAT invoices in the UAE, this concerns you.

Why the UAE is Introducing Electronic Invoicing

The introduction of the UAE electronic invoicing guidelines aligns with global tax modernization efforts. Countries across Europe and the GCC have implemented structured invoice reporting systems to improve tax transparency and reduce fraud.

From a regulatory standpoint, the objectives are clear: to strengthen VAT compliance, reduce invoice manipulation, enable near real-time transaction monitoring, and improve audit efficiency.

The framework complements the VAT regime administered by the Federal Tax Authority (FTA), which already imposes penalties for non-compliance under Federal Decree-Law No. 8 of 2017 on VAT.

This is not about adding paperwork. It is about digitizing transaction validation at the source.

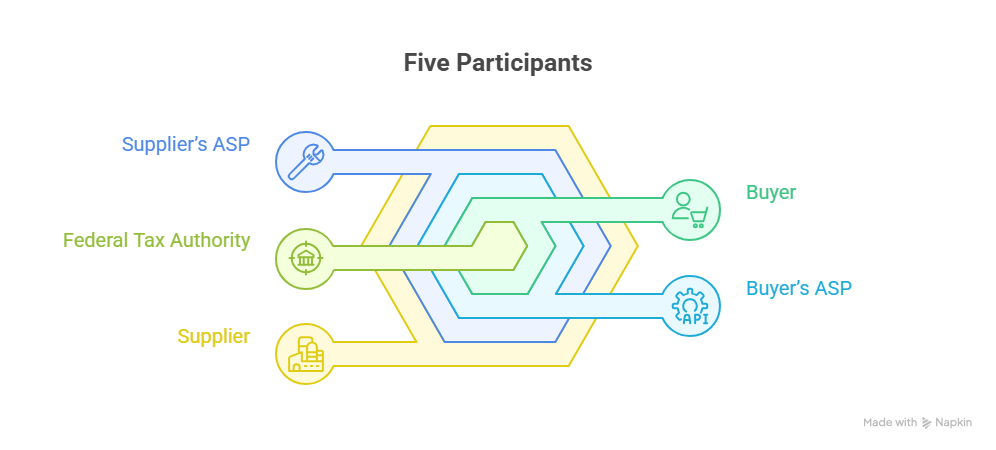

Understanding the UAE’s 5-Corner Model

The UAE has adopted a decentralized continuous transaction control model, commonly called the “5-corner model.” The five participants are:

Unlike centralized clearance systems, invoices are exchanged through accredited private service providers who ensure validation and reporting.

In practical terms:

- The supplier generates a structured invoice (XML format).

- The invoice is transmitted to their ASP.

- The ASP validates it for compliance and required data fields.

- The invoice data is reported to the authority in near real time.

- It is then transmitted to the buyer via interoperable networks.

The biggest operational shift here is the timing. Under the traditional model, errors could sometimes be corrected at month-end before VAT filing. Under structured reporting, validation happens at the transaction level. That compresses the margin for error.

What Actually Changes for Businesses

1. Structured Invoice Format is Mandatory

PDF invoices alone will not meet compliance standards once the mandate is enforced.

Invoices must:

- Follow a structured XML schema

- Include mandatory VAT fields

- Contain unique identifiers

- Be transmitted through an accredited ASP

Expert insight: Based on our advisory work, one recurring issue is poor master data management. Customer VAT numbers, addresses, and invoice numbering inconsistencies may not surface today, but under automated validation, they will trigger rejections.

2. Accredited Service Providers (ASPs) are Required

Businesses must integrate their ERP or accounting systems with an ASP authorized under the framework.

This is a critical control point. During the selection of an ASP, consider:

- System compatibility

- API capability

- Data security protocols

- Archiving solutions

- Validation reporting features

Expert advice: We strongly recommend involving both IT and finance teams in this evaluation. Too often, system selection is left to one department.

3. Near Real-Time Reporting to the Authority

Transaction visibility increases significantly. This change means:

- Delayed corrections become riskier

- Backdated adjustments may attract scrutiny

- Process discipline becomes essential

Under UAE penalty structures, procedural violations can result in administrative fines. Ensuring reporting accuracy from day one reduces long-term risk.

Case Study: Data Readiness Gaps in a Logistics Company

Last year, we advised a mid-sized logistics operator preparing for international digital reporting compliance.

During the system testing, we identified duplicate invoice numbering sequences, manual credit note issuance outside the ERP, incorrect VAT mapping on domestic freight, and incomplete customer TRN validation.

If such weaknesses existed under real-time reporting, invoice rejection rates would likely exceed 20% during initial rollout, similar to patterns seen in early adoption phases in other jurisdictions.

We conducted a structured data-cleansing exercise and an ERP reconfiguration. Within eight weeks, reconciliation discrepancies reduced by 32%, VAT filing accuracy improved, and audit documentation improved significantly.

Expert insight: Compliance preparation often reveals operational inefficiencies that were previously hidden.

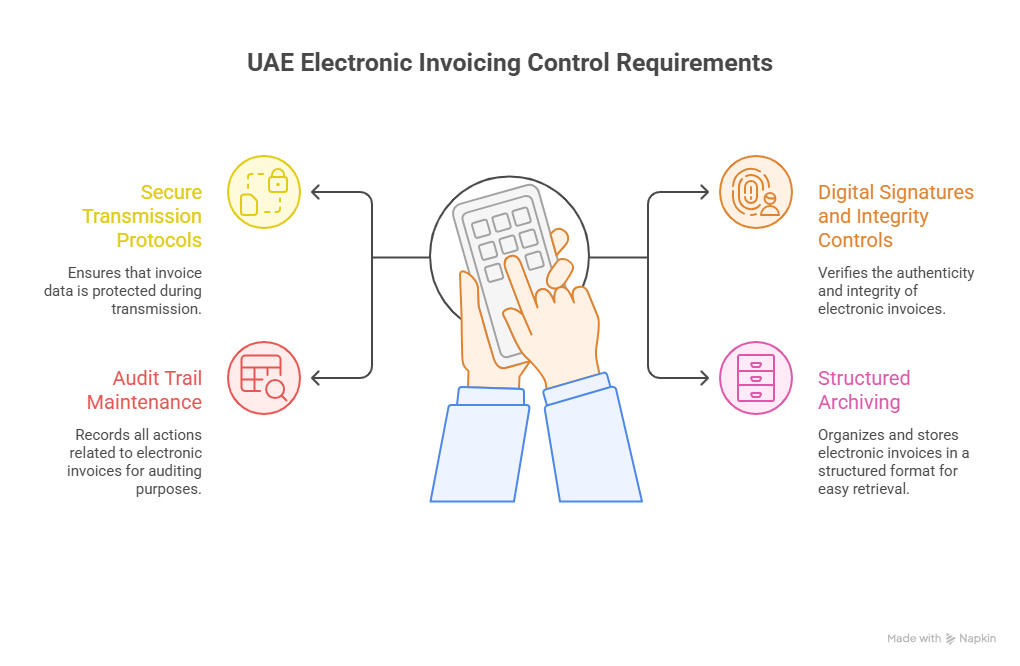

Technical and Governance Implications

The UAE electronic invoicing guidelines introduce several control requirements:

This is no longer purely an accounting matter. It requires collaboration between the finance, IT, compliance, and internal audit departments.

Governance frameworks should be reviewed to ensure invoice issuance authority, credit note approvals, and system access controls are clearly documented.

Businesses that treat this as a cross-functional project adapt far more smoothly than those that isolate it within the finance teams.

Risks of Delayed Preparation

Waiting until enforcement dates are finalized may expose businesses to ERP upgrade bottlenecks, limited ASP availability, cash flow disruptions due to invoice rejections, penalty exposure, and operational strain.

VAT implementation in 2018 demonstrated a clear pattern: businesses that began preparing 12–18 months early experienced significantly fewer compliance gaps. The same principle applies here.

Strategic Opportunities Beyond Compliance

While many view E-invoicing as a regulatory burden, there are potential benefits too, including automation of reconciliation processes, reduction in manual input errors, improved reporting analytics, stronger audit readiness, and reduced fraud risk.

- Expert experience: One manufacturing client we advised during VAT system upgrades reduced manual reconciliation hours by nearly 40% once structured controls were embedded into their ERP.

Compliance can drive operational improvement when approached strategically.

What Businesses Should Do Now

Based on the issued framework and practical implementation experience, companies should:

- Conduct a system readiness assessment

- Review invoice data quality

- Map VAT logic within ERP systems

- Shortlist potential accredited service providers

- Allocate budget for integration and testing

- Train finance and IT teams

Early-stage review typically identifies system design weaknesses that may not be visible during routine operations.

UAE’s New E-Invoicing System Explained: Ministry of Finance Policy Breakdown & Business Impact with RadiantBiz

When preparing for the UAE’s new e-invoicing framework, compliance is about far more than simply adjusting invoice formats or integrating new software.

Many business owners underestimate how structured reporting requirements will affect cash flow timing, VAT accuracy, system validation, and long-term operational stability, challenges we have already seen businesses experience.

In our experience, the most common risks arise when companies approach e-invoicing as a purely technical upgrade without fully assessing ERP compatibility, transaction volume, data accuracy, credit note frequency, and regulatory reporting exposure.

Much like banking decisions, compliance infrastructure choices made at the early stage can either support growth or create avoidable complications later.

At RadiantBiz, we take a structured advisory approach. Before recommending an Accredited Service Provider or integration pathway under the framework issued by the UAE Ministry of Finance, we review your business model, invoice workflows, VAT mappings, and expected reporting obligations.

This ensures that your systems are not only compliant with the FTA's requirements but also scalable as your operations expand.

Selecting the wrong integration strategy can lead to invoice rejections, payment delays, validation errors, or the need to reconfigure systems after implementation, risks that often cost far more than proper preparation at the outset.

We saw similar patterns during VAT implementation, where businesses that rushed system changes later faced avoidable reconciliation problems and audit stress.

By combining regulatory expertise with practical implementation planning, RadiantBiz helps UAE businesses transition smoothly into structured e-invoicing, protect liquidity, and strengthen internal controls.

FAQs

1. When will the UAE electronic invoicing mandate take effect?

The implementation is expected to be phased. VAT-certified businesses should monitor official publications from the Ministry of Finance and Federal Tax Authority for final enforcement timelines.

2. Will PDF invoices still be allowed?

Once the structured mandate becomes active, standalone PDFs will not meet compliance standards. Invoices must follow a structured electronic format transmitted via accredited service providers.

3. Are free zone companies required to comply?

If a free zone company is VAT-certified and making taxable supplies, it is likely to fall within the scope of the framework, subject to implementation details.

A Structural Shift in Transaction Reporting

The announcement that the UAE Ministry of Finance has issued new electronic invoicing guidelines signals a structural modernization of the country’s VAT framework.

This is not a cosmetic update. It changes how invoices are created, validated, transmitted, and archived.

Over the decade of advising UAE businesses through VAT implementation, regulatory audits, and ERP integration projects, we can confidently say:

The organizations that act early reduce risk, protect cash flow, and build stronger compliance cultures.

Now is the time to evaluate your readiness, not when enforcement deadlines are announced. Seek our professional on-the-ground guidance, contact us via mail at info@radiantbiz.com, WhatsApp, or call us at +971521322895!

Anjali Jawahar ensures the seamless execution of business setup processes, making compliance and licensing effortless for clients. Her keen attention to operational efficiency helps the RadiantBiz businesses establish themselves smoothly in the UAE.

.avif)