2.png)

Why Bank Account Applications Get Rejected in the UAE (And How to Fix it)

Table of Contents

About the Author

The author is a UAE banking consultant with over 15 years of experience in the financial sector. He has worked with leading regional and international banks, advising more than 15,000 startups and SMEs on corporate structuring, bank onboarding, and regulatory positioning.

Key Takeaway:

- Banks assess risk under AML/CFT frameworks, checking KYC, beneficial ownership, business model, and transaction flow. A rejection usually signals gaps in documentation, source of funds, or business substance rather than the business being inherently “bad.”

- Applications are often declined due to inconsistent documents, unclear capital origin, lack of UAE business presence, unrealistic projections, or high-risk industry classification. Addressing these before submission greatly improves approval chances.

- Businesses should audit documents, clarify the source of funds, ensure logical and credible transaction flow, and align operations with UAE residency/substance requirements. After correcting issues, applying to banks suited to the business sector increases the likelihood of success.

Why Your UAE Corporate Bank Account May Be Rejected (Even If Everything Looks Perfect)

Opening a corporate bank account in the UAE should be simple. You have your trade license. Your visa is stamped. Your office is set up. Clients are ready. Then the email arrives:

“We regret to inform you…”

If you’ve faced a bank account rejection in the UAE, you’re not alone. And more importantly, it doesn’t mean your business is flawed.

After over a decade working in UAE banking and advising startups and SMEs, we can confidently say this: most rejections happen because founders underestimate compliance requirements, not because banks are randomly turning down businesses.

In this article, we’ll explain why UAE banks reject applications, what really happens inside compliance departments, real case studies based on our experience, and how to fix and avoid rejection the right way.

Understanding How UAE Banks Actually Assess You

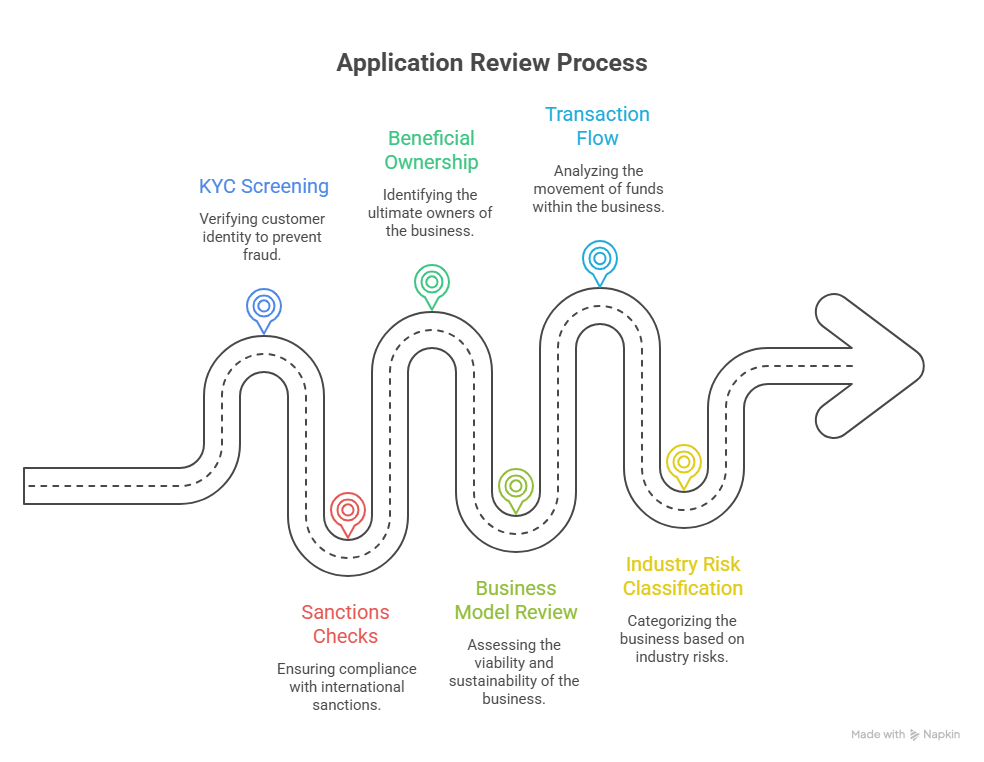

Before we talk about rejections, you need to understand something critical: Banks in the UAE do not “open accounts.” They assess risk.

Under the supervision of the Central Bank of the United Arab Emirates, financial institutions must follow strict Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) frameworks.

The UAE has also strengthened oversight following evaluations by the Financial Action Task Force. When your application is submitted, it goes through:

If compliance officers cannot clearly understand what you do, who you deal with, where your money comes from, and how funds will move. They will decline your application.

This is not personal, it’s procedural.

The Most Common Reasons for Bank Account Rejection in UAE Cases

From reviewing hundreds of onboarding files over the years, these are the most frequent triggers.

1. Inconsistent or Incomplete Documentation

This is the number one issue. Typical problems include:

- The trade license says “consultancy,” but the business plan describes trading

- Shareholder name is slightly different across the passport and the license

- MOA activity is not aligned with the revenue model

- No clarity on Ultimate Beneficial Owner (UBO)

We’ve seen applications declined because a middle name was missing on one document.

Expert tip: Conduct a full documentation audit before submission. Align every document with your actual business model.

2. Unclear Source of Funds

If you are injecting capital, banks must understand its origin. They may request:

- Personal bank statements

- Property sale agreements

- Tax returns

- Financial statements

- Dividend certificates

Expert experience: A client transferred AED 700,000 ($190,606) to the UAE after selling property overseas. The bank rejected the file due to insufficient source documentation. We submitted the property sale contract, transfer proof, and tax clearance confirmation. Approval followed within two weeks. Transparency reduces suspicion.

3. Lack of UAE Business Substance

This issue is common among free zone companies. Banks assess:

- Do you have a physical office or only a flexi-desk?

- Are shareholders UAE residents?

- Do you have local contracts?

- Does your website look operational?

If everything suggests offshore activity routed through a UAE entity, compliance flags it.

Expert experience: An EU entrepreneur incorporated a company in Dubai but continued operating from abroad, without a UAE visa, office lease, or local clients. His application was rejected by three banks. After relocating to the UAE, securing office space, and signing local contracts, the fourth bank approved the account. This demonstrates that business substance matters.

4. High-Risk Industry Classification

Some industries are subject to Enhanced Due Diligence (EDD), such as cryptocurrency, precious metals, cross-border trading, NGOs, and large-volume import/export.

With the introduction of the Virtual Assets Regulatory Authority (VARA) in Dubai, digital asset businesses face even closer scrutiny. This doesn’t mean automatic rejection. It means deeper questioning.

Expert tip: Apply to banks with a known appetite for your sector and provide detailed transaction mapping.

5. Unrealistic Transaction Projections

This is more common than people think.

If your startup capital is AED 50,000 ($13,614.7) but your forecast shows $10 million annual turnover, compliance will question credibility.

Banks evaluate logical consistency. Based on our experience, aligning projected revenue with signed contracts dramatically improves credibility.

6. Shareholder Risk Profile Issues

Banks run internal screenings for sanctions exposure, Politically Exposed Person (PEP) status, adverse media, and previous account closures.

Many founders don’t realize that prior account issues in the UAE can affect future applications. Honesty is critical. Declare concerns upfront rather than letting compliance discover them independently.

Case Studies from Our Practice

To make this practical, here are structured examples.

Case Study 1: General Trading Company Rejected Twice

Problem: License said “General Trading.” No clear specialization.

Bank Concern: Vague trading often implies risk of third-party fund routing.

Solution: We restructured the model to electronics accessories only, submitted supplier agreements, buyer contracts, and realistic projections.

Outcome: Approved within 21 days.

Case Study 2: Consultancy With No UAE Residency

Problem: Two foreign shareholders. No Emirates ID. Working remotely.

Bank Concern: Shell company risk.

Solution: Secured residency visas, physical office lease, and local client contract.

Outcome: Approval after resubmission.

Case Study 3: Crypto Advisory Firm

Problem: No documented regulatory alignment.

Bank Concern: Sector under enhanced regulatory review.

Solution: Provided a compliance framework, regulatory position clarity, and transaction explanation.

Outcome: Approved by sector-aligned bank.

What Happens After a Bank Account Rejection in the UAE?

Many assume rejection equals blacklisting. In most cases, the rejection is internal to that specific bank, other banks may still consider you, and you can reapply after restructuring.

However, repeated applications without fixing root issues increase perceived risk. Pause. Diagnose. Correct. Then reapply.

Our Professional Framework Before Submitting Any Application

After years in this field, we personally check three core areas before any submission:

1. Business Activity Consistency

Does the license match actual revenue sources?

2. Defensible Source of Funds

Can we prove exactly where capital originated?

3. Logical Transaction Flow

If I were compliance, would I approve this?

If any of these fail, we restructure before submission. This dramatically reduces the risk of bank account rejection in the UAE.

Common Myths About Bank Account Rejection in the UAE

Myth: Once rejected, you are blacklisted.

Reality: Most rejections are internal to one institution.

Myth: Free zone companies always get rejected.

Reality: Risk profile matters more than jurisdiction.

Myth: Bigger deposit guarantees approval.

Reality: Source transparency matters more than amount.

How to Fix a Rejection the Right Way

If you’ve already faced a bank account rejection in the UAE, follow this structured approach:

- Identify the likely trigger (documentation? substance? projections?)

- Gather additional supporting evidence

- Adjust your business narrative

- Select a bank suited to your sector

- Submit a clean, coherent file

Do not rush into another submission without adjustments.

Why Bank Account Applications Get Rejected in the UAE (And How to Fix it) with RadiantBiz

When discussing why bank account applications get rejected in the UAE, most business owners focus only on missing documents or high-risk activities. In reality, rejection risks often begin much earlier, at the operational and compliance structuring stage.

Banks assess far more than your trade license. They review transaction logic, revenue consistency, VAT reporting alignment, projected cash flow, and whether your internal controls match your stated business model. When systems are loosely structured or financial reporting lacks clarity, it raises red flags during onboarding or enhanced due diligence.

At RadiantBiz, our banking consultants regularly see rejections occur because businesses treat compliance as an afterthought rather than as an infrastructure. Much like choosing the wrong corporate structure something our business setup consultants in Dubai address from day one — weak financial foundations can delay approvals or trigger ongoing monitoring.

Our advisory approach evaluates your business model, reporting flow, and banking profile before submission. This ensures your company presents a credible, transparent, and scalable risk profile, significantly improving approval outcomes while protecting long-term banking stability.

FAQs

1. Why does bank account rejection in the UAE happen so often?

UAE banks operate under strict AML regulations and international oversight. Any inconsistency, high-risk indicator, or unclear source of funds can result in rejection.

2. Can I apply to another bank after being rejected?

Yes. Rejection from one bank does not automatically block you elsewhere. However, correct the underlying issues first.

3. Does having a free zone company increase rejection risk?

Not inherently. Rejection depends on business substance, activity clarity, and risk profile, not simply the licensing jurisdiction.

Rejection is a Compliance Signal, Not Failure

After advising hundreds of businesses over the past decade, we can say this with confidence: Most rejections are preventable. Banks are not looking to reject good businesses. They are looking to avoid regulatory exposure.

If your documentation is aligned, your source of funds is transparent, your projections are realistic, and your structure is credible, approval becomes far more likely.

Treat the account opening process as a compliance exercise, not an administrative step. And if you’ve already experienced a bank account rejection in the UAE, view it as feedback — not defeat.

Correct the structure. Strengthen the file. Apply strategically. Seek our professional on-the-ground guidance, contact us via mail at info@radiantbiz.com, WhatsApp, or call us at +971521322895!

%20.webp)

.webp)

Shariq Ansari specializes in banking solutions and regulatory compliance. His experience with UAE banks enables businesses to navigate complex financial and compliance challenges efficiently.

.avif)