2.png)

Fintech and MAS Licensing in Singapore: What You Need to Know Before Incorporating

.webp)

Table of Contents

About the Author

Our business setup consultant writes this article with over a decade of experience helping entrepreneurs establish companies in Singapore and the UAE. Having worked with startups, SMEs, and international investors, they have guided businesses through jurisdiction selection, tax structuring, and banking strategies across both regions.

Key Takeaway:

- Incorporating a company with ACRA does not equate to regulatory approval; fintech founders must identify their specific business activities to secure the correct MAS license (PSA, CMS, or DTSP) before accepting customer funds to avoid enforcement action.

- With a historical approval rate under 3% for digital payment licenses, applicants must demonstrate substantial paid-up capital, appoint qualified Compliance Officers, and satisfy strict "Fit and Proper" criteria for all directors.

- Securing a license typically takes 6–12 months and requires a budget of SGD 250,000–500,000 ($185,000–$370,000) for readiness, making early engagement with regulatory counsel and consideration of the Regulatory Sandbox essential for success.

The 3% Reality: Why Most Fintech Applications Fail in Singapore

Singapore approved just 14 of the more than 500 digital payment license applications it received in the years following the Payment Services Act, a clearance rate under 3%. The door to fintech in Singapore is still open in 2026, but it now opens for a very specific kind of applicant.

If you are reading this, you are likely standing at the starting line. You might assume that company formation in Singapore is your first move - incorporating with ACRA and getting the paperwork filed. It isn't. Your first step is understanding fintech licensing in Singapore.

Get this wrong, and you could waste months of runway, or face enforcement action before you launch a product.

We've guided dozens of founders through this maze. Some succeeded because they treated compliance as a core strategy, others stalled because they viewed it as bureaucracy. This guide maps the path from idea to licensed operator based on today's market reality.

Note: All prices are estimates based on market rates at the time of publication. Actual costs may vary due to daily exchange rate fluctuations and potential bank transfer fees.

Why Fintech Licensing in Singapore Demands a Strategy Before Setup

Fintech licensing in Singapore is activity-based, not entity-based. Your business model dictates your license, not your company name.

Can a Foreigner Own 100% of a Fintech Company in Singapore?

Yes, Singapore permits 100% foreign ownership of a Private Limited company, with no nationality restrictions on shareholders. You must appoint at least one locally resident director, a Singapore citizen, PR, or EntrePass holder. For MAS-regulated entities, the resident director must show genuine involvement and substance, not act as a nominee.

ACRA Incorporation vs. MAS Authorization: Knowing the Difference

Incorporating a Private Limited company with ACRA is not the same as getting a license from MAS.

Think of ACRA as the DMV that issues your car license. MAS is the traffic authority that decides whether you may operate a bus, taxi, or cargo truck. You can own the vehicle (your company), but operating a payment platform without the right permit will get you pulled over.

Many founders rush through company incorporation and corporate bank account opening with a corporate secretarial firm, thinking the job is done. Six months later, they realise they cannot legally accept customer funds.

Before filing incorporation documents, identify your activity. Each of these triggers a different regulatory requirement:

- Moving money (account issuance, domestic and cross-border transfers)

- Storing customer value (e-money issuance, prepaid wallets)

- Managing investments on behalf of clients

- Trading or dealing in digital payment tokens

- Providing financial advice or distributing investment products

Do You Always Need a MAS License to Start a Fintech in Singapore?

Not every fintech needs a MAS license, only those carrying out regulated activities under the Payment Services Act, Securities and Futures Act, or Financial Advisers Act.

If you are building B2B SaaS, KYC infrastructure, or pure technology layers without holding customer funds, you can operate without a license.

The moment you touch customer money, issue tokens, or recommend investments, licensing becomes mandatory.

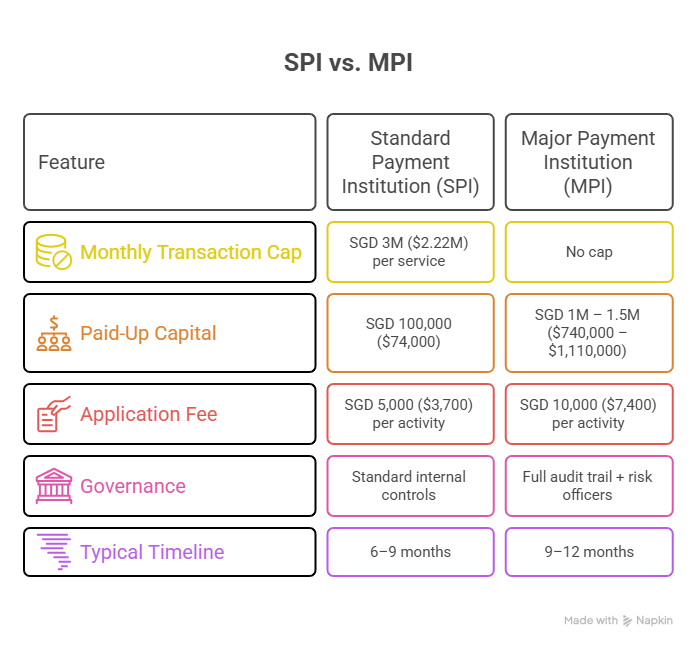

Payment Services Act 2019: SPI vs. MPI License Requirements Explained

For most startups, the Payment Services Act (PSA) is the law to know. If you are building an e-wallet, a remittance service, or a crypto exchange offering digital payment token services, you are looking at a Standard Payment Institution (SPI) or a Major Payment Institution (MPI) license.

SPI vs. MPI License: What is the Difference?

Here is how the two payment license tiers compare:

Expert experience: We worked with a founder who built a cross-border remittance app targeting Southeast Asian migrant workers and needed a cross-border remittance license. He assumed he was small enough to fly under the radar. He launched a beta with 500 users and processed SGD 2 million ($1.48 million) in his first quarter.

Within three months, he hit the volume cap. MAS flagged him. He had to pause operations, scramble to upgrade his compliance infrastructure, and apply for the MPI license retroactively. It cost him a quarter of his funding and delayed his Series A.

If your projections show you'll quickly exceed SGD 3 million ($2.22 million) monthly, plan for the MPI route from day one.

Capital Markets Services (CMS) License for Fund Managers and Robo-Advisors

Some founders aren't moving cash, they're moving securities, derivatives, or managing portfolios. If your fintech involves advising clients on investments, executing trades, or managing a Variable Capital Company (VCC) fund structure, you fall under the Securities and Futures Act, requiring a CMS license.

MAS distinguishes between managing your own money and managing others'. Pooling investor funds to invest on their behalf requires a CMS license for fund management.

Watch out for the "exempt" trap. While the Accredited Investor exemption and other carve-outs exist under the SFA, they are narrow. Soliciting the public, even online, likely crosses the line.

Digital Token Service Provider (DTSP) Licensing Under the FSM Act

A major shift took effect on 30 June 2025, when MAS activated the DTSP regime under the Financial Services and Markets Act 2022.

If your Singapore-incorporated entity offers digital token services to customers outside Singapore, even with no local customers, you now require a DTSP license.

This closes the long-standing offshore crypto loophole. The regime imposes strict AML/CFT obligations, capital requirements, and a high bar: MAS will license only applicants with strong governance and clear use cases.

Founders building global crypto products from Singapore must factor DTSP licensing into their structure from day one.

MAS Regulatory Sandbox: How to Test Your Fintech Before Full Licensing

If full licensing feels overwhelming, the Regulatory Sandbox is a controlled environment where you can test innovative products with real customers without the full licensing burden.

We recommend it for any startup with novel technology or a model that doesn't fit existing categories. The Sandbox lets you validate tech, gather feedback, and prove your case to investors while working closely with regulators.

Don't treat it as a permanent home. It's a launchpad with strict time limits and exit conditions.

Singapore Corporate Tax and Tax Incentives for Licensed Fintechs

Singapore charges a flat 17% corporate tax rate, but new companies benefit from the Start-Up Tax Exemption, 75% off the first SGD 100,000 ($74,000) of chargeable income and 50% off the next SGD 100,000 ($74,000) for the first three years.

Licensed fintechs may also qualify for the Financial Sector Incentive scheme, offering concessionary rates of 5% to 13.5% on qualifying income.

From January 2025, Singapore implemented the Domestic Top-up Tax in line with OECD Pillar Two rules, affecting multinational groups with global revenues above EUR 750 million.

Weigh these against the UAE and Hong Kong alternatives early.

Fit and Proper Criteria, Paid-Up Capital, and Compliance Officer Requirements

MAS doesn't just look at your code, they look at your people. Every director and key executive must pass a "Fit and Proper" background check: no criminal records, no regulatory breaches, and relevant experience.

MAS wants to see that leadership understands AML/CFT compliance, cyber threats, and market volatility risks. You need a seasoned Compliance Officer and a Money Laundering Reporting Officer (MLRO).

Paid-up capital requirements are not just a number on a balance sheet; the funds must be liquid and available. It sits there as part of client money safeguarding rules, acting as a safety net for customers.

For an MPI, that can mean locking up over a million dollars before your first sale.

How Much Does it Cost to Get a MAS License?

The application fee for an SPI is SGD 5,000 ($3,700), and for an MPI is SGD 10,000 ($7,400) per activity.

The real expense lies in paid-up capital (SGD 100,000 ($74,000) to SGD 1.5 million ($1,110,000)), Compliance Officer salaries (SGD 120,000 ($88,000) to SGD 200,000 ($148,000) annually), legal advisory fees, and audit costs.

Budget SGD 250,000 ($185,000) to SGD 500,000 ($370,000) for end-to-end readiness before operational runway.

Why MAS License Applications Get Rejected (And How to Avoid it)

The rules are also tightening. MAS now expects compliance with the Travel Rule for crypto, the Technology Risk Management (TRM) guidelines, and mandatory incident reporting within one hour of a breach.

Build your architecture without these in mind, and you will have to tear it down and rebuild it.

Top three rejection reasons we've seen:

- Weak board composition: Directors who cannot demonstrate a clear understanding of financial crime risks.

- Inadequate capital planning: Showing that paid-up capital will be depleted by operational costs before approval.

- Vague business plans: Proposals lacking a clear revenue model or sustainability path.

Compliance is not a back-office function. It is a competitive advantage.

When you pitch to institutional partners or enterprise clients, a MAS license signals trust. In a market flooded with fly-by-night operators, that trust is your most valuable asset.

Fintech and MAS Licensing in Singapore with RadiantBiz

Before incorporating a fintech in Singapore, determine if your activities fall under MAS regulation. Licensing is a separate, post-incorporation process, failure to secure the right license will halt operations.

RadiantBiz handles your Singapore company incorporation, official address, resident director appointment, and corporate bank account introductions so your structure is correct from day one, making the MAS license application smoother.

You'll need separate regulatory counsel for the MAS filing itself, incorporation gets you ready, and MAS licensing lets you legally operate.

FAQs

1. How long does it take to get a fintech license in Singapore?

An SPI takes 6–9 months. An MPI or CMS license takes 9–12 months or longer. Delays occur when applications need clarifications or additional background checks on key personnel.

2. Can I operate while my license application is pending?

Generally, no, operating a regulated financial service without a license is a criminal offence. You can participate in the MAS Regulatory Sandbox under specific exemptions and must communicate clearly that you are in testing.

3. What is the minimum capital for a fintech license?

SPI: SGD 100,000 ($74,000). MPI: SGD 1 million to SGD 1.5 million ($740,000 to $1,110,000). CMS: from SGD 250,000 ($185,000) for fund management, higher for capital markets dealing. Always check current MAS guidelines.

Final Word: Building a Licensed Fintech in Singapore

Singapore remains the premier destination for fintech in Asia, but "move fast and break things" is over. The new mantra is "move smart and build trust."

Is Singapore Still the Best Fintech Hub in Asia in 2026?

Singapore continues to lead Asia for fintech in 2026, supported by MAS's Project Guardian for tokenization, the Finance for Net Zero Action Plan, and ongoing initiatives like the Financial Services Industry Transformation Map 2025.

%20.webp)

%20(1).webp)

.webp)

%20.webp)

Anjali Jawahar ensures the seamless execution of business setup processes, making compliance and licensing effortless for clients. Her keen attention to operational efficiency helps the RadiantBiz businesses establish themselves smoothly in the UAE.

.avif)