2.png)

Structure d'une société holding à Singapour : comment l'utiliser pour se développer dans la région Asie-Pacifique

Table des matières

À propos de l'auteur

Notre consultant en création d'entreprise rédige cet article fort d'une expérience de plus de dix ans dans l'accompagnement d'entrepreneurs souhaitant créer leur société à Singapour et aux Émirats arabes unis. Ayant travaillé avec des start-ups, des PME et des investisseurs internationaux, il a aidé de nombreuses entreprises à choisir leur juridiction, à mettre en place leur structure fiscale et à définir leurs stratégies bancaires dans ces deux régions.

Point à retenir :

- Establishing a Singapore holding company creates a "corporate firewall" that isolates operational risks in volatile APAC markets while leveraging a network of 90+ Double Taxation Agreements (DTAs) and a single-tier dividend system to minimize withholding taxes and eliminate capital gains tax.

- To maintain treaty benefits and comply with OECD BEPS standards (especially post-2025 Pillar Two reforms), the entity must demonstrate genuine economic substance, including local directors, physical office presence, and strategic decision-making in Singapore, rather than operating as a "brass plate" shell.

- Singapore serves as an ideal Regional Treasury Center (RTC) due to the absence of foreign exchange controls, allowing for the seamless consolidation of regional profits, intra-group financing, and global capital deployment without the repatriation hurdles found in markets like China or India.

Why Singapore Holding Company Formation Drives Asia-Pacific Expansion

Entering Asia-Pacific (APAC) without a robust corporate structure is not a cost-saving move, it is a hidden liability. The World Bank consistently ranks Singapore among the world's top jurisdictions for ease of doing business, but its real value lies in functioning as a strategic holding hub.

A properly structured Singapore holding company formation, often functioning as a regional headquarters (RHQ), is not merely a compliance exercise but a critical financial and legal instrument.

For CFOs and founders, the decision should be driven by specific metrics: access to 90+ Double Taxation Agreements (DTAs), a single-tier dividend tax system, and a regulatory environment aligned with OECD BEPS standards.

Remarque : tous les prix sont des estimations basées sur les taux du marché en vigueur au moment de la publication. Les coûts réels peuvent varier en raison des fluctuations quotidiennes des taux de change et des éventuels frais de virement bancaire.

Strategic Architecture: How a Singapore HoldCo Centralizes Control and Limits Liability

The core advantage is the separation of ownership from operations. The holding company (HoldCo) stays in Singapore while operating subsidiaries (OpCos) sit in target markets like Vietnam, Indonesia, or India.

Whether structured as a private limited company or a variable capital company (VCC) for fund holding purposes, it centralizes intellectual property, optimizes cash flow through treaty networks, and isolates liability across jurisdictions.

What are the Requirements to Set Up a Holding Company in Singapore?

A Singapore holding company requires at least one shareholder, one locally resident director, a qualified company secretary appointed within six months of incorporation, an official local address, and a minimum paid-up capital of SGD 1 ($0.74).

Foreigners may own 100% of the shares. All entities must incorporate with ACRA and file annual returns.

How Much Does it Cost to Set Up a Singapore Holding Company?

ACRA incorporation fees are SGD 315 ($233.1), including name reservation.

Total first-year costs typically range from SGD 3,500 to SGD 8,000 ($2,590 to $5,920) once nominee director services, company secretary services, physical address, and basic accounting are factored in.

Larger structures with treasury or IP functions may incur SGD 15,000 to SGD 25,000 ($11,100 to $18,500) annually.

For a full breakdown beyond holding structures, see our complete Singapore company formation cost guide.

How long does it take to incorporate a Singapore Holding Company?

Standard ACRA incorporation takes 1 to 3 business days. Full setup, including corporate bank account opening and resident director appointment, typically takes 4 to 6 weeks. Bank account opening is now the longest stage, as DBS, OCBC, and UOB conduct enhanced due diligence on beneficial owners.

Expert experience: A European fintech expanded into Southeast Asia in 2022 through a single Indonesian entity. When Indonesian data localization rules tightened, the entire group's IP and cash were exposed. Restructuring through Singapore moved IP to the HoldCo and reduced the Indonesian entity to a service provider. The next regulatory friction cost only the OpCo's capital, saving an estimated $4.5 million.

Singapore Corporate Tax Efficiency: Beyond the 17% Headline Rate

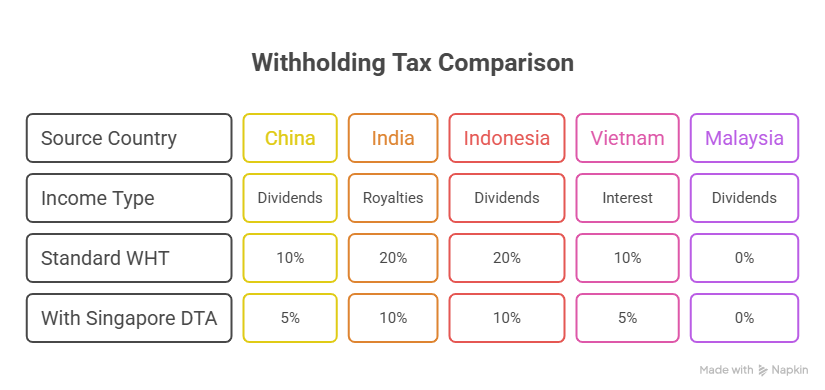

Singapore's 17% corporate tax rate is competitive, but the real value lies in its DTA network and participation exemption regime.

These treaties enable withholding tax exemption or significant reductions on dividends, interest, and royalties flowing from operating subsidiaries back to the Singapore HoldCo.

Singapore also operates a single-tier tax system. Dividends paid by a Singapore company to its shareholders are tax-free in the recipient's hands.

The foreign-sourced income exemption (FSIE) takes this further, dividends, branch profits, and service income received from overseas are tax-exempt in Singapore, provided the foreign income was taxed at a headline rate of at least 15%.

Is Singapore a Good Jurisdiction for a Holding Company?

Yes, Singapore is consistently ranked among the world's top three jurisdictions for holding company formation.

Key advantages include 90+ DTAs, zero capital gains tax, a single-tier dividend system, no foreign exchange controls, and a legal environment based on English common law.

It is particularly favoured for APAC operations because it offers OECD-compliant substance rules without the reputational baggage of traditional tax havens.

Are Dividends Received by a Singapore Holding Company Taxed?

Dividends received from foreign subsidiaries are generally exempt under FSIE, provided the income was taxed at a headline rate of at least 15% in the source country.

Dividends paid out by the Singapore HoldCo to its shareholders are also tax-free, regardless of shareholder residence.

Expert insight: Treating the DTA as automatic is the most common error. To claim treaty benefits, the Singapore entity must demonstrate substance, local board, board meetings held in Singapore, and key decisions made locally. IRAS actively audits for shell companies.

Treasury Management and Cross-Border Capital Mobility in APAC

Capital mobility is a primary constraint across APAC. China, Vietnam, and India maintain strict foreign exchange controls. A Singapore holding company solves this by acting as a Regional Treasury Center (RTC), a status that also qualifies for concessionary tax rates under the Finance & Treasury Centre incentive scheme.

Singapore has no foreign exchange controls and no capital gains tax. Profits can be repatriated as dividends, consolidated, and deployed globally without restriction. This enables:

Centralized cash management

Consolidating regional liquidity to negotiate better bank rates

Intra-group financing

Lending capital to subsidiaries at arm's length rates to optimise interest deductions

Currency hedging

Using Singapore's deep derivatives markets to hedge FX risk across APAC

Expert experience: One manufacturing client consolidated cash from Thai, Malaysian, and Philippine subsidiaries through their Singapore RTC, cutting external borrowing costs by 1.2% annually.

Economic Substance and BEPS Compliance Requirements for Singapore Holding Companies

Jurisdictions offering "brass plate" companies are under intense scrutiny. Singapore has adapted, requiring genuine economic substance for holding companies.

To maintain treaty benefits, your Singapore HoldCo must:

- Employ sufficient qualified staff locally

- Maintain a real physical presence

- Hold board meetings in Singapore with strategic decision-making done locally

- Complete ACRA incorporation properly, maintain accounting records, and file annual returns

2026 Update: Pillar Two, Refundable Investment Credit, and Substance Reforms

Singapore implemented the Income Inclusion Rule and Domestic Top-up Tax (DTT) on 1 January 2025, aligning with the OECD's Pillar Two 15% global minimum tax for groups with revenue above €750 million.

To offset this, the Refundable Investment Credit (RIC) scheme offers qualifying companies up to 50% support on capital, manpower, and R&D expenditure.

Smaller holding companies below the Pillar Two threshold retain the 17% headline rate and partial exemptions, including the Singapore startup tax exemption scheme for qualifying new companies. IRAS now requests evidence of local decision-making during tax filings, not only on audit.

Future-Proofing Your Structure for IPO, M&A, and Investor Exits

Investors and acquirers, including those entering Singapore through the Global Investor Programme (GIP), prioritize clean, transparent structures.

A Singapore top-co simplifies due diligence for SGX listings or trade sales to US and European buyers. Buyers will scrutinize intercompany agreements and transfer pricing documentation to ensure profits were not artificially shifted.

Singapore vs. UAE Holding Company: Which Suits Your APAC Strategy?

Both jurisdictions offer 0% capital gains tax, strong DTA networks, and 100% foreign ownership. Singapore wins for pure APAC operations through proximity, investor familiarity, and the SGX listing pathway.

The UAE, through DIFC, ADGM, or mainland Dubai, wins for groups also serving MEA, South Asia, and Europe, offering 9% corporate tax and Golden Visa eligibility for founders.

Many sophisticated groups now use a dual-hub model: a Singapore HoldCo for APAC OpCos and a UAE entity as the global parent.

We break the full decision down in our Singapore vs Dubai company formation comparison.

Singapore Holding Company Formation with RadiantBiz

RadiantBiz acts as your embedded corporate infrastructure team. We handle the ACRA enrollment, fulfil the resident director requirement, and design the entire governance framework to satisfy IRAS substance requirements from day one.

Our team, including tax partners and legal experts, structures intercompany agreements, sets up regional treasury capabilities, and prepares transfer pricing documentation before you generate your first dollar of revenue.

We bridge Singapore and UAE expertise so groups planning multi-jurisdictional expansion get one coordinated structure, not two disconnected entities.

Foire aux questions

1. What is the minimum paid-up capital for a Singapore holding company?

No statutory minimum, a company can incorporate with SGD 1 ($0.74). For banking and substance purposes, SGD 50,000 to SGD 100,000 ($37,000 to $74,000) is often recommended, especially for treasury or asset-holding functions.

2. How does the Global Minimum Tax (Pillar Two) impact Singapore holding companies?

Pillar Two introduces a 15% global minimum corporate tax rate. Multinationals with revenue above €750M ($825M) may pay a top-up tax through Singapore's Domestic Top-up Tax. Smaller companies are generally unaffected.

3. Can a Singapore holding company own assets in other countries without subsidiaries?

Technically, yes, but inadvisable, direct ownership of foreign assets can trigger permanent establishment risks and local tax exposure. A local subsidiary isolates liability and ensures sector ownership compliance.

Building Long-Term Value Through the Right Singapore Holding Structure

A Singapore holding company is a foundational element providing legal protection, tax efficiency, and operational agility.

Success depends on adherence to substance requirements and rigorous compliance, and as global tax regulations tighten, the value of a well-structured Singapore entity only increases.

Recommended next steps:

- Conduct a jurisdictional risk assessment for your target markets

- Engage qualified corporate secretary services to handle Singapore holding company formation and ongoing ACRA filings

- Develop a transfer pricing policy aligned with OECD guidelines

- Establish a local board and physical presence to satisfy substance requirements

Ready to design your APAC structure? Seek our professional on-the-ground guidance, contact us via mail at info@radiantbiz.com, WhatsApp, or call us at +971521322895!

%20.webp)

%20(1).webp)

.webp)

%20.webp)

Fort de plus de 15 ans d'expérience dans le secteur bancaire et du conseil aux entreprises, Rizwan Ansari dirige RadiantBiz avec pour objectif de simplifier la création d'entreprise aux Émirats arabes unis.

.avif)