2.png)

Virtual Banks for Hong Kong Companies: Options Compared

Table of Contents

About the Author

Our business setup consultant writes this article with over a decade of experience helping entrepreneurs establish companies in Hong Kong and the UAE. Having worked with startups, SMEs, and international investors, they have guided businesses through jurisdiction selection, tax structuring, and banking strategies across both regions.

Key Takeaways:

- Unlike the 3–6 week, high-rejection process of 2016, licensed virtual banks in 2026 allow non-resident directors to open fully functional business accounts remotely in under 48 hours via video KYC, provided they submit clean documentation regarding source of funds and operational substance.

- While virtual banks (like ZA, WeLab, and Livi) excel at high-velocity transactions, low fees, and API integrations for daily operations, they currently lack capabilities for complex trade finance (e.g., Letters of Credit), therefore, the recommended strategy for 2026 is a hybrid approach using a virtual bank for daily cash flow and a traditional bank for long-term reserves and specialized instruments.

- There is no single "best" bank; founders should choose based on their specific use case, ZA Bank for scaling SMEs needing SWIFT and APIs, WeLab or Livi for cost-efficient FX and CNY trade, Mox for embedded credit lines, and Airstar for same-day payroll, to maximize efficiency and minimize costs.

From Paper Forms to Digital Onboarding: Hong Kong Business Banking in 2026

In 2016, opening a corporate bank account in Hong Kong as a non-resident took three to six weeks, four banker meetings, and a 60% chance of rejection. By 2026, founders are clearing the same hurdle in under 48 hours from a laptop in Dubai or London. This shift is the story of Hong Kong's virtual banks, and choosing the wrong one still costs founders thousands.

Today the game has completely changed. Licensed virtual banks, authorized by the Hong Kong Monetary Authority, have turned banking from a bureaucratic hurdle into a digital experience.

But with seven major players competing for your business, choosing the wrong one can cost as much as sticking with the old guard. This guide cuts through the noise based on a decade of advising clients on Hong Kong company incorporation and banking.

Whether you run a tech startup, an e-commerce store, or a freelance consultancy needing an Electronic Money Institution (EMI) for Hong Kong business operations, you will see exactly where your money should sit.

Note: All prices are estimates based on market rates at the time of publication. Actual costs may vary due to daily exchange rate fluctuations and potential bank transfer fees.

Are Virtual Banks Safe? HKMA Licensing and Deposit Protection Explained

Before the bank-by-bank breakdown, the question we hear weekly: are these digital banks safe? The answer is in the license.

All seven virtual banks in Hong Kong are licensed by the Hong Kong Monetary Authority (HKMA) under the same Banking Ordinance as traditional banks. They are subject to the same capital adequacy requirements, liquidity ratios, and AML compliance checks expected of any licensed Hong Kong bank.

A key trust factor is that funds held with any licensed virtual bank fall under the same Deposit Protection Scheme (DPS) that covers up to HKD 500,000 ($64,267) per depositor per bank.

There is one structural nuance. Virtual banks often partner with traditional banks for underlying deposit infrastructure, which is why we always advise a hybrid strategy: a virtual bank for high-velocity transactions and a traditional bank for long-term reserves.

How Hong Kong's 2026 AML Updates Affect Virtual Bank Onboarding

The Hong Kong Monetary Authority tightened its AML compliance expectations in early 2026, requiring all licensed virtual banks to apply enhanced due diligence on cross-border corporate accounts.

For non-resident applicants, this means more granular questions about the source of funds, the operational substance of your Hong Kong company, and the nature of your end clients.

Banks now request supporting evidence such as supplier contracts, recent invoices, or a website domain matching your trading activity. Founders who prepare these materials in advance still complete onboarding in 48 to 72 hours.

Those who treat the application as a form-filling exercise face follow-up requests that stretch the process to two weeks or trigger outright rejection.

Can a Non-Resident Open a Hong Kong Business Bank Account Remotely?

Yes. Non-resident directors can complete remote account opening with most virtual banks in Hong Kong, including ZA Bank, WeLab, and Livi.

You will need a valid passport, your Hong Kong business license certificate, recent proof of address, and a short business description.

A live video KYC verification call usually replaces any in-person visit. Traditional banks still prefer face-to-face meetings, which is why digital-first banks now dominate non-resident applications.

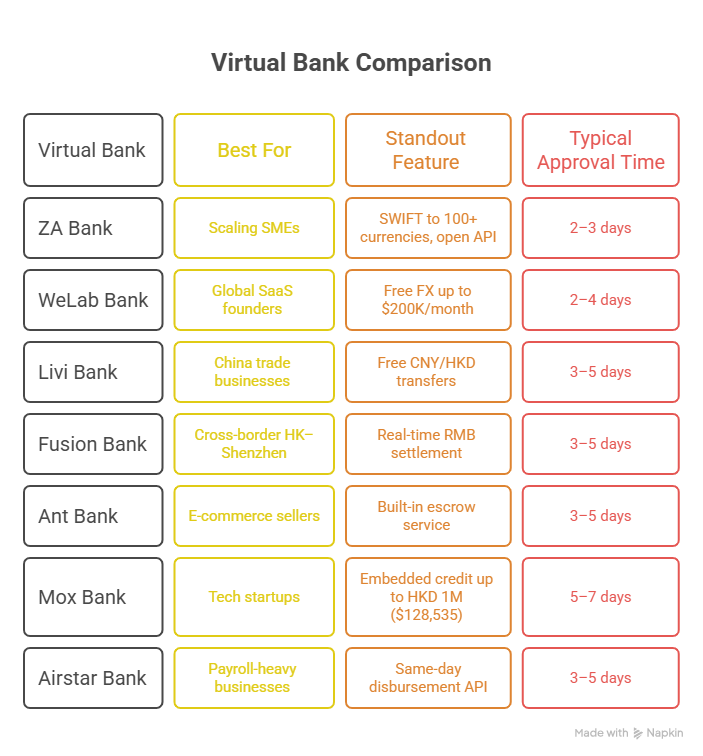

ZA Bank: Best Virtual Bank in Hong Kong for Scaling SMEs and SWIFT Payments

ZA Bank is my consistent recommendation for operational scale. They were the first virtual bank in Hong Kong to report a monthly profit in 2024, a sign of a sustainable model rather than a venture-burn strategy.

Expert experience: A Central-based software house with 40 employees was drowning in manual reconciliation on a traditional bank account that charged HKD 150 ($19.28) per wire with no API. We migrated their operating account to ZA Bank and used their open API banking integration to connect directly to Xero and automate their payroll runs. They cut admin time by 15 hours a week and saved roughly HKD 45,000 ($5,784) a year in wire fees.

ZA Bank offers a zero-fee multi-currency business account supporting HKD, USD, CNY, and GBP, with a soft balance ceiling of HKD 10 million ($1,285,347). The standout feature is SWIFT outbound coverage across 100+ currencies, critical for hardware importers and overseas-payroll teams.

Expert tip: ZA's onboarding is fully digital, non-resident directors only need a valid passport and a current business license certificate to begin verification. Mismatched address formats are the most common rejection trigger.

How Long Does it Take to Open a Virtual Bank Account in Hong Kong?

Most licensed virtual banks in Hong Kong approve a complete application within 2 to 5 business days, with some accounts going live in under 48 hours.

Speed depends on the quality of your submission. Clean documents, a clear shareholder structure, and a director ID matching your business license certificate move you to the front of the queue.

Complex structures involving offshore holding companies typically extend the review to 7 to 10 business days.

WeLab Bank vs Livi Bank: Low-Fee Virtual Accounts for Startups and CNY Trade

Not every business needs a HKD 10 million ($1,285,347) ceiling. For early-stage founders and freelancers, the priority is keeping costs at zero.

WeLab Bank is our go-to for SaaS companies with international revenue. The fee-free basic business account includes unlimited local payments, and the killer feature is free FX at interbank rates up to $200,000 monthly.

Livi Bank dominates cross-border payments along the CNY/HKD corridor. For trade with mainland China, Livi offers free cross-border transfers between CNY and HKD.

Expert experience: A small textile importer was losing 1.5% on every CNY conversion with a traditional bank. Shifting their primary settlement to Livi Bank saved them around HKD 120,000 ($15,424) in their first year, pure margin restored.

What is the Minimum Deposit for a Hong Kong Virtual Bank Account?

Most Hong Kong virtual banks require zero minimum deposit to open and maintain a business account. ZA Bank, WeLab, and Livi all advertise no minimum balance for their core SME tier.

Traditional banks still expect HKD 10,000 to HKD 50,000 ($1,285 to $6,427) as an opening deposit, plus monthly fees if balances dip below the threshold.

Fusion Bank and Ant Bank: Cross-Border RMB Settlement and E-Commerce Escrow

Sometimes a generalist won't do. Fusion Bank participates in the Shenzhen-Hong Kong cross-border data validation pilot, enabling real-time settlement of RMB-linked invoices, a game-changer for HK businesses with Shenzhen manufacturing partners.

Ant Bank, backed by Ant Group, offers digital escrow specifically built for e-commerce sellers. It adds a layer of trust that standard accounts lack.

Expert warning: If you have international investors, disclose your banking partners. Some stakeholders have specific compliance preferences around Ant Group given the geopolitical landscape.

Mox Bank and Airstar Bank: Embedded Credit and Same-Day Payroll for Hong Kong Startups

Mox Bank offers an embedded "Pay-Later" credit line of up to HKD 1 million ($128,535) subject to credit assessment. For a startup that needs a working capital loan to bridge invoicing and payment, this is invaluable, no separate lender required.

Airstar Bank, launched in late 2024, targets payroll-heavy businesses with free same-day disbursement and an API for real-time payment notifications.

Expert experience: A recruitment agency was losing two days on payroll clearing. After integrating with Airstar, Friday-afternoon runs landed in employee accounts by Monday morning at zero fees. Payroll-related satisfaction scores rose 30%.

Comparison Table: Hong Kong Virtual Banks at a Glance

Limitations of Virtual Banks: Trade Finance, Support, and Integration Gaps

No physical branches

Complex trade finance like Letters of Credit and collateralized lending still require a traditional bank partner.

Customer support latency

Support is digital-first, urgent 2 a.m. issues rarely reach a human immediately.

Integration limits

Test the API connection with your specific (Enterprise Resource Planning) ERP before migrating your primary account.

Virtual Banks vs Traditional Banks in Hong Kong: 2026 Comparison

Virtual banks now match or beat traditional banks on speed, fees, and digital integration, but they are still building parity on lending.

A traditional bank like HSBC or Hang Seng remains the right choice for letters of credit, trade finance, and large secured facilities.

Virtual banks lead on remote account opening, multi-currency business accounts, and API connections to Xero or QuickBooks.

The practical 2026 setup for most founders is a primary virtual bank account for daily operations and a secondary traditional account reserved for trade instruments or institutional reserves.

How to Choose the Right Virtual Bank for Your Hong Kong Company

Volume and velocity

High transaction count with low average value points to WeLab or ZA Bank.

Currency mix

Heavy CNY exposure favours Livi or Fusion, heavy USD or EUR exposure favours ZA Bank.

Credit needs

If you need an embedded working capital loan, Mox Bank's Pay-Later facility is the strongest fit.

Payroll focus

Larger teams with strict timing benefit from Airstar's same-day disbursement.

Which is the Cheapest Virtual Bank in Hong Kong for SMEs?

WeLab Bank is generally the cheapest for SMEs with international revenue thanks to free FX up to $200,000 monthly and zero local payment fees.

Livi Bank wins on cost for businesses focused on the CNY/HKD corridor.

ZA Bank becomes competitive once volumes scale, but WeLab's interbank FX rate typically delivers the lowest all-in cost for the average exporter.

Virtual Banks for Hong Kong Companies with RadiantBiz

At RadiantBiz, we work with founders who treat banking as core infrastructure, not paperwork. After years guiding startups through Hong Kong's regulatory landscape, our recommendation is clear: integrate a licensed virtual bank into your financial stack.

Traditional banking creates bottlenecks with weeks-long onboarding and opaque fee structures. Virtual banks like ZA Bank, WeLab, and Livi let our clients launch fully functional accounts in under 48 hours– speed that translates directly into revenue.

Beyond cost, the real edge is digital integration: robust APIs that connect to Xero, QuickBooks, and payroll systems, automating reconciliation and giving real-time visibility into cash flow.

Whether you need a full corporate bank account or a streamlined EMI for a Hong Kong business solution, our banking consultants help you find the best virtual bank HK company has to offer.

FAQs

1. Are virtual banks in Hong Kong safe for business accounts?

Yes. All seven licensed virtual banks are HKMA-regulated under the same prudential rules as traditional banks.

2. Can I open a virtual bank account for my Hong Kong company if I live overseas?

Yes, most virtual banks, ZA Bank, WeLab, and Livi, allow remote onboarding for non-resident directors.

3. What is the difference between a virtual bank and an Electronic Money Institution (EMI) for Hong Kong business?

A virtual bank is a licensed bank that accepts deposits and is insured under DPS. An EMI like Statrys or Aspire holds funds in safeguarded accounts but generally cannot lend or pay interest.

Choosing Your Hong Kong Virtual Bank: Final Recommendations

The days of waiting weeks for business account approval are over.

Hong Kong's virtual banks are faster, cheaper, and more flexible, choose ZA Bank for infrastructure, WeLab for FX savings, or Ant Bank for e-commerce tools depending on your needs.

If you aren't ready to switch your primary relationship, open a secondary virtual account first. Test the API. Experience the speed.

Your business deserves a banking partner that moves as fast as you do, and RadiantBiz is here to help you make the right call.

Seek our professional on-the-ground guidance, contact us via mail at info@radiantbiz.com, WhatsApp, or call us at +971521322895!

Shariq Ansari specializes in banking solutions and regulatory compliance. His experience with UAE banks enables businesses to navigate complex financial and compliance challenges efficiently.

.avif)